The contents below were directly copied/pasted from this SEC report submitted by Yandex @ https://www.sec.gov/Archives/edgar/data/1513845/000110465919064935/a19-23249_1ex99d2.htm

The only change is to highlight several sections in green, yellow and red that should be reviewed by policy makers based on escalating priority levels.

………….

LETTER FROM OUR CHAIRMAN

November 18, 2019

Dear Shareholders,

I am pleased to introduce this Shareholder Circular for Yandex N.V. in relation to two shareholder meetings to be held on Friday, December 20, 2019 starting at 10:00 a.m. CET: a meeting of the holders of the Class A Shares and, immediately following the Class A Meeting, an Extraordinary General Meeting of all shareholders. At these two meetings, we will ask our shareholders to approve a restructuring of the corporate governance structure of the Yandex Group (the “Restructuring”).

Since our inception two decades ago, we have aspired to set the highest standards for corporate governance. We are especially proud of the careful consideration we have always given to the interests of all our stakeholders, particularly our public shareholders.

I am writing to explain the background to and reasons for the proposed Restructuring and why the Board considers the proposed Restructuring to be in the best interest of Yandex and all of its stakeholders, including in particular the Class A Shareholders. The Board thought long and hard and worked closely with management and external advisors before recommending this set of modifications to the Company’s governance structure.

These modifications allow us to address the fundamental issues facing the Company today. Specifically, we believe we have dealt with key concerns of the public authorities in our principal market, as well as issues relating to “single-man risk”, without affecting our day-to-day business and operations or long-term prospects. We believe we have cleared the path for continued growth and success.

This is why the Board unanimously recommends that Yandex shareholders vote in favor of the proposed Restructuring at the Class A Meeting and the Extraordinary General Meeting.

In this Shareholder Circular, we provide you with information regarding the proposed Restructuring. We advise all our shareholders to carefully read this and other related documents for further information.

We are proposing the Restructuring in light of regulatory and legislative developments in Russia, which is our principal market. The Board and management of Yandex carefully monitor the political and regulatory environment in which the Company operates, and maintain a regular dialogue with relevant government stakeholders about Yandex’s role in the Russian economy and society. As you know, our success has allowed our core business to grow into an ecosystem that serves tens of millions of consumers and businesses in Russia and beyond that collects and stores vast amounts of personal data of our users. We have developed cutting-edge intellectual property and other technology that serve as the backbone of our products and services. During the course of 2018 and 2019, it became clear that Russian authorities had concerns about foreign influence over this strategically important business. We believed that these concerns created a serious risk for the Company, evident in ongoing consideration of potential restrictions on foreign ownership of businesses in our sector.

In response to these developments, the Board created a Special Committee in October 2018, consisting solely of independent non-executive directors, to assist the Board in considering and evaluating potential courses of action. The Special Committee sought to identify mechanisms to address concerns in Russia’s developing regulatory environment, while preserving the continuity of our business and our ability to advance our evolution as a global leader in technology and innovation. In carefully considering a broad range of strategic options, the Special Committee developed and recommended, and the Board approved, the proposal for the Restructuring laid out in this Shareholder Circular, with the goal of ensuring the ongoing success of Yandex and protecting the interests of all of its stakeholders, including in particular the Class A Shareholders, consistent with our duties as directors of a Dutch company. This was a rigorous process that we believe explored all feasible alternatives to achieve the aims I have just laid out.

The changes we are proposing are targeted in nature and we believe are proportionate to achieving these aims. The Board fully endorses them, believing that this is the best option for enabling Yandex to balance a number of competing demands, including:

· the interests, financial and otherwise, of our Class A Shareholders;

· the public interests in our principal market;

· the need for the business to attract and retain talent;

· the interests of our users in the continued development of our offerings; and

· the overall continuity of our business.

I will be voting my shares in favor of the proposed Restructuring, and I hope that you will too, so that we can focus on what we all want: supporting Yandex’s continued development as a world-class technology leader with a growing portfolio of innovative products and services, and a focus on maximizing long-term shareholder value.

Shareholder Meetings

The notice, agenda and explanatory notes for the Shareholder Meetings are set out below and are available at https://ir.yandex/shareholder-meetings. If you would like to cast your votes by proxy at either meeting, you will have to do so in any event no later than 11:59 p.m. (Amsterdam time) on December 19, 2019. Please see the Notice of Meeting for details.

To implement the proposed Restructuring, an amendment of the Articles of Association is required. Such amendment requires both a majority of at least three-quarters (3/4) of the votes cast in the Class A Meeting, and a majority of at least two-thirds (2/3) of the votes cast at the EGM.

All votes are important to us and I urge you to cast your vote.

The Shareholder Meetings present an important opportunity for all Yandex shareholders to express their views by asking questions about the proposed Restructuring and related resolutions. If you are planning to attend the Shareholder Meetings in person we ask that you please provide advance notice by notifying us at EGM2019@yandex-team.ru before 5.30 p.m. (Amsterdam time) on December 17, 2019. If you would like to be assured of the fullest possible response to a question asked during either of the Shareholder Meetings, it would be helpful if you could give me prior notice of your question. Of course, you are also invited to write to me at YNVchairman@Yandex-team.ru at any time should you wish.

I look forward to seeing as many of you as possible there.

Yours sincerely,

John Boynton

Chairman of the Board

LETTER FROM OUR CEO

November 18, 2019

Dear Shareholders,

Over the past year, our Board has been conducting a rigorous process to evaluate the evolving environment in which we operate, to examine and anticipate potential challenges facing our business — regulatory and otherwise — and to proactively find solutions aimed at ensuring our future success in the interests of all of our stakeholders.

John Boynton, our Chairman, has outlined some of the wider context and why we felt it was important to address these issues. I would just add some additional context from my perspective as founder and CEO of this business.

Since we started Yandex 22 years ago, we have grown and transformed it into one of the world’s largest and most innovative technology companies. We are developing breakthrough ideas and innovating across multiple platforms and services in a way that will shape the future of the technology sector — not just in Russia but around the world.

This is an exciting time for our business. We have built a scaled ride-sharing business that is both rapidly growing and profitable. We have developed one of the leading self-driving car technologies in the world. And we continue to develop around our search business, mapping, streaming music, cloud and so much more — the possibilities are endless.

Today we have an ecosystem that touches the daily lives of millions of people in Russia. We also collect and are responsible for securely storing personal data of millions of Russian users. The intellectual property we own is significant and sensitive enough to be a potential concern for national security. The same goes for some of our core technology.

As a result, we also have this great responsibility to protect and safeguard public interests in a way that is both targeted and measured.

This is why I urge our shareholders to support the proposals we are announcing today. It is what we need to do so that we can focus on what we do best — innovating, providing world-class products and services to our users, and delivering superior returns to our investors. I will be voting my shares in favor of the proposed Restructuring, and I hope that you will too.

To demonstrate my commitment and belief in the Company’s future, I have agreed to a lock-up agreement covering 95% of my Class B shares until January 1, 2022.

I urge all our shareholders to read this Shareholder Circular carefully for further information about our plans.

Thank you for your continued support and I look forward to hearing from many of you over the coming weeks.

Yours sincerely,

Arkady Volozh

Chief Executive Officer

1. INTRODUCTION AND SUMMARY

Introduction

Below we describe the proposed Restructuring and why the Board is asking you to approve the proposals set out in this Circular. Our Board members are required under Dutch law to take into account the interests of all of our stakeholders, including our users, employees and the broader community in which we operate — as well as our shareholders. Our Board believes that the proposed Restructuring is in the best interests of the Company and the enduring success of its business and of all its stakeholders, including in particular our Class A Shareholders.

To implement the proposed Restructuring, an amendment of the Articles of Association is required. Such amendment requires both a majority of at least three-quarters (3/4) of the votes cast in the Class A Meeting, and a majority of at least two-thirds (2/3) of the votes cast at the EGM.

Background

Over the past 22 years, Yandex has grown tremendously, transforming into one of the world’s most innovative technology companies and the leader in our home market, Russia. Our broad ecosystem of services touches many areas of daily life in Russia, affecting tens of millions of users. We are a unique and highly strategic constituent of the Russian economy and play a critical role in the broader community in which we operate.

While Yandex is the leading search provider in Russia, it is also much more than that. When people compare us with the big international players, they often call us the Russian Google, Uber, Waymo, Amazon and Spotify combined. Our audience equals the total number of Internet users in Russia – more than 100 million people a month, most of whom use Yandex services several times a day. Users ask Yandex more than 7 billion search queries per month. Our voice assistant, Alice, responds to more than a billion requests monthly. Every day, people listen to more than 265 years of audio and more than 58 million tracks on Yandex.Music. Yandex.Taxi completes more than 100 million trips every month.

More than a million Russians also derive some or all of their income with the help of the Yandex ecosystem. More than 700,000 drivers and couriers connect to our Yandex.Taxi and Yandex.Food apps, for example, while more than a million people contribute to our Yandex.Toloka crowd-sourced task platform. At the same time, we not only create technological services and products, but also develop educational projects, with more than a million children and adults learning with Yandex services.

In common with our international peers, we operate in a rapidly evolving environment of increasing scrutiny of technology companies by policymakers, regulators and the consumers alike. Indeed, the trend towards increasing scrutiny of technology businesses is not confined to any one country or region. Politicians and regulators across the globe are grappling with how best to ensure that the increasing reach and influence of technology companies can best serve the interests of users and the public. Although these concerns are still emerging, it is clear that the security of data and intellectual property is a key issue. These same concerns have become pronounced in Russia in recent years.

The Board has been particularly mindful of proposed new legislation that would restrict foreign influence on companies that provide internet services and collect user data in Russia. Accordingly, our Board has been considering how best to address these concerns while safeguarding the interests of our public shareholders, providing a framework for strong corporate governance and ensuring that the unique culture and growth potential of the Company are preserved. The Board has therefore developed the proposals described in this document (the “Restructuring”) with a view to addressing these concerns in a targeted and proportionate manner.

The Restructuring has a number of different features. Although these proposals entail a degree of complexity, they have been carefully calibrated to preserve our strong current governance structure. The proposals would create a structure that enables a new body that will represent a broad set of public interests in Russia, which we call the Public Interest Foundation, to have a direct or indirect say in specified and targeted matters in respect of our operations in Russia, such as the Company’s ability to provide direct access to personal data of Russian users to foreign persons, or dispose of material intellectual property.

As technology and our business continue to evolve, the regulatory environment will likely continue to evolve as well. As a consequence, additional concerns may arise that we may need to address. It is possible that the proposed Restructuring may not address all future concerns as to foreign influence over Russian internet and technology companies. We will continue to monitor the Company’s position and if we conclude that further steps are required to protect the interests of our stakeholders, including in particular our Class A Shareholders, we may return to shareholders for further approvals.

It is important to note that the Restructuring does not affect the economic rights of the Class A Shares. Indeed, the proposed amendment to the Articles of Association would provide the Class A Shareholders with additional rights. Separate Class A Shareholder approval will be required for:

· the transfer of the enterprise or substantially all of the enterprise of Yandex to a third party;

· the conclusion or cancellation of any long-lasting cooperation by Yandex or a subsidiary with any other legal person or company or as a fully liable general partner of a limited partnership or a general partnership, provided that such cooperation or the cancellation thereof is of essential importance to Yandex;

· the acquisition or disposal of a participating interest in the capital of a company with a value of at least one-third of the sum of the assets according to the consolidated balance sheet in the most recently adopted set of annual accounts of Yandex, by Yandex or a subsidiary;

· entering into of any transaction or series of related transactions by Yandex or a subsidiary involving (i) the payment of an amount in excess of one-third of the sum of the assets according to the consolidated balance sheet in the most recently adopted set of annual accounts of Yandex, or (ii) the sale of assets with a value in excess of the amount set forth in (i) above; and

· the issuance of shares in excess of 20% of our issued share capital.

Summary of Changes to Corporate Governance

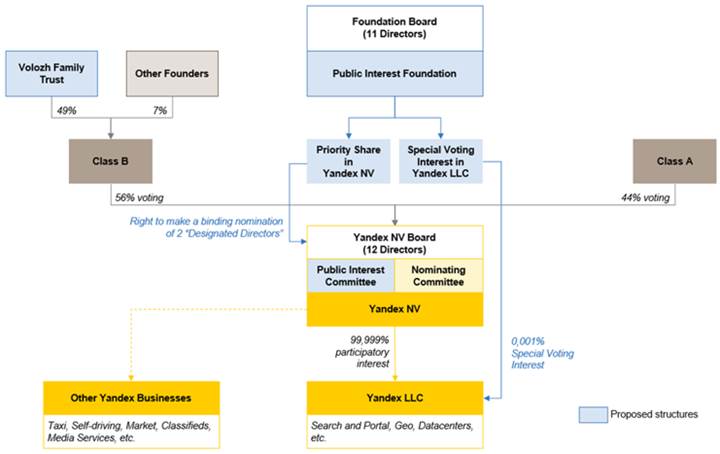

We have designed the proposed Restructuring as a targeted approach to addressing the core public interest concerns we have identified, as well as the specific “single-man” risk arising as a result of Mr. Volozh’s concentrated holding of voting power. The proposed structure includes elements at the levels of both Yandex N.V., the parent company of our group, and Yandex Russia, our principal operating subsidiary in Russia, which holds, directly or indirectly, most of our material intellectual property, data centers and our core business, including search and portal.

Public Interest Foundation and Designated Directors

The Public Interest Foundation is a key element of the Restructuring and is designed to address the public interest concerns we have identified. The statutory purpose of the Foundation, as set out in its charter, will be to preserve the continuity and promote the success of the Yandex Group business. The Public Interest Foundation will be incorporated in the Oktyabrskiy special administrative region in Kaliningrad, in the Russian Federation, under a new legislative framework that is similar to the Dutch foundation structure (the so-called “stichting”), which is a widely-used feature of Dutch law. The draft legislation was approved by the State Duma in its third reading on November 13, 2019, and is expected to be considered by the upper chamber of the Russian parliament, the Federation Council, in the coming weeks and if approved, to be submitted to the President of the Russian Federation for signature by the end of 2019.

The Public Interest Foundation will have no shareholders, owners or beneficiaries, and will be governed by the Foundation Board. The Foundation Board will have 11 members, to consist initially of five directors to be appointed by specified Russian universities, three directors to be appointed by specified non-governmental Russian institutions, and three members of Yandex management. The Company has an established and productive working relationship with each of these universities and non-governmental Russian institutions (details of which are set out below) that will have a right to appoint a director to the Foundation Board.

The Public Interest Foundation will hold a Priority Share in the Company, allowing it to make binding nominations of two Designated Directors (out of a total of 12 directors). Under Dutch law, a binding

nomination will be adopted at a General Meeting of shareholders, unless rejected by a two-thirds (2/3) majority of those voting.

The Priority Share will also give the Public Interest Foundation an effective veto over the acquisitions of stakes greater than 10% in our Company, or the sale of our material business, as described below.

Through the nomination of Designated Directors, the Public Interest Foundation will have indirect control over material decisions related to providing direct access to personal data of Russian users to foreign persons, or disposing of material intellectual property.

Through the Designated Directors, the Public Interest Foundation will also have a right of veto over candidates to be nominated for election to four of the seats on our Board. Therefore the Foundation will have a direct or indirect say in the composition of half of our 12 person Board. In addition, the election of the General Director of Yandex Russia in the ordinary course will require the Board to vote by a special majority of eight (as may be adjusted for any Board vacancies) including at least one vote of the Designated Directors. If a candidate to the position of General Director is rejected five times due to the absence of the affirmative vote of the Designated Director, the Board may approve the candidate by the special majority of nine (as may be adjusted for any Board vacancies).

The Public Interest Foundation will also hold a Special Voting Interest in Yandex Russia with a right to replace the General Director on a temporary basis in certain exceptional situations described below.

The Priority Share is currently held by Sberbank. The existing Priority Share provides the holder with the right:

· to approve the accumulation by a party, group of related parties or parties acting in concert, of the legal or beneficial ownership of shares representing 25% or more, in number or by voting power, of the outstanding Class A and Class B Shares (taken together), if the Board has otherwise approved such accumulation of shares; and

· to approve a decision of the Board to sell, transfer or otherwise dispose of, directly and indirectly, all or substantially all of our assets to one or more third parties in any transaction or series of related transactions, including the sale of Yandex Russia.

It is proposed that the existing Priority Share will be transferred to the Public Interest Foundation and its terms will be amended to provide the new holder with the following rights (with the new provisions in bold italics):

· to approve the accumulation by a party, group of related parties or parties acting in concert, of the legal or beneficial ownership of shares representing 10% or more, in number or by voting power, of the outstanding Class A and Class B Shares (taken together), if the Board has otherwise approved such accumulation of shares. The accumulation threshold will be lowered from 25% (as it currently is) to 10%;

· to approve a decision of the Board to sell, transfer or otherwise dispose of, directly and indirectly, all or substantially all of our assets to one or more third parties in any transaction or series of related transactions, including the sale of Yandex Russia; and

· to make binding nominations of two Designated Directors, as described above.

The Priority Share does not carry any rights to control the management or operations of the Company, and its economic rights are limited to its pro rata nominal entitlement to dividends and other distributions (a maximum distribution of one eurocent annually).

Special Voting Interest

As additional support for the protective rights of the Public Interest Foundation, we propose to issue to the Public Interest Foundation a Special Voting Interest in Yandex Russia. The Special Voting Interest will allow the Public Interest Foundation to temporarily replace the General Director of Yandex in certain exceptional circumstances, a list of which will be set out in the publicly available charter of Yandex Russia and are described in detail below. We believe that the issuance of the Special Voting Interest in Yandex Russia, giving the Public Interest Foundation the right in certain defined and targeted circumstances to exert control over the management of our principal Russian operating subsidiary, will effectively provide comfort to the public authorities that this protective structure is not entirely reliant on resolution outside of Russia.

Public Interest Committee

The Public Interest Committee will be a new committee of the Board. It will consist of three members: the Yandex CEO and both of the Designated Directors. Importantly, decisions of the Public Interest Committee may only be taken unanimously. The Public Interest Committee will not review ordinary business or commercial matters. Its right of approval will be limited to a defined list of specific matters related to the provision of direct access to personal data of Russian users to foreign persons, or disposal of material intellectual property. The Board cannot act in respect of any of the Public Interest Committee’s specified matters prior to receiving a recommendation from the Public Interest Committee. The Public Interest Committee will act only as a check on the Board’s actions; it cannot proactively make any decisions on behalf of the Board.

Amendment to the Class B Shares; Volozh Family Trust

As part of the proposed Restructuring, we are also proposing an amendment to the automatic conversion feature of the Class B Shares. Currently, such shares would immediately convert into Class A Shares upon the death of the holder, including Mr. Volozh. To avoid this “cliff edge” scenario, in which the voting control of the Company could suddenly shift, the amendment would provide that Class B Shares held by a family trust would not automatically convert until the end of a period of two years following the holder’s death, at which point the shares will automatically convert into Class A Shares. Mr. Volozh intends to establish a family trust in connection with the Restructuring, which will agree, during the two-year period following Mr. Volozh’s death, to vote the Class B shares it will hold in favor of any proposals made by our Board and otherwise in accordance with the recommendations of the Board. These measures are intended to ensure an orderly transition period, and are similar to the structures that have been adopted by other public technology companies such as Crowdstrike, Dropbox, Lyft, Pinterest and Snap.

Lock-up Agreement

Mr. Volozh and the Volozh Family Trust intend to enter into a lock-up agreement in favor of the Company with respect to 95% of the Class B Shares currently held by Mr. Volozh, pursuant to which they will undertake not to dispose of such shares prior to January 1, 2022. Even if the other holders of Class B Shares were to sell their shares and Mr. Volozh were to sell up to 5% of his Class B Shares, as permitted under his lock-up agreement, he would still hold over 51% of votes in the Company and, as such, control would remain in Russian hands during this period.

Mr. Volozh is not currently subject to any lock-up restriction in respect of his Class B Shares. He has agreed that he, and his family trust, will enter into such restriction to demonstrate his commitment to the Company and provides an additional layer of assurance that there will be no abrupt change in the voting structure of our Company.

The lock-up agreement will provide that such restrictions may be waived or released by our Board, acting by a supermajority of eight (8) directors, subject to adjustment in the case of Board vacancies.

Overview of the Proposed Restructuring

Current Corporate Governance Structure

Currently, Yandex has three classes of authorized ordinary shares in issue: Class A Shares, with one vote per share, Class B Shares, with ten votes per share and Class C Shares, with nine votes per share; as well as one Priority Share. The Class B Shares are held by Arkady Volozh and other members of our founding team, and together have approximately 56% of the voting power of our equity shares. This structure was introduced before Yandex’s initial public offering in 2011, and was designed to ensure that our founding management continued to exercise voting control even after they ceased to hold a majority of our issued shares, thereby enabling them to focus on the long-term interests of our Company. Our Class C Shares serve only to facilitate the conversion of our Class B Shares into Class A Shares under Dutch law. For the limited period of time during which Class C Shares are outstanding, they are voted by a Dutch foundation that holds these shares in the same proportion as the votes by holders of our Class A Shares and Class B Shares, so as not to influence the outcome of any vote.

We originally issued our Priority Share in September 2009 to Sberbank for its nominal value of €1.00. The Priority Share currently affords the holder the right to approve the accumulation by a party, group of related parties or parties acting in concert, of the legal or beneficial ownership of shares representing 25% or more, in number or by voting power, of the outstanding Class A and Class B Shares (taken together), if the Board has otherwise approved such accumulation of shares. Yandex shareholders approved the decision to issue the Priority Share to Sberbank with the objective of strengthening the control over the Company’s ownership structure and providing transparency with respect to changes in ownership.

Any decision by the Board to sell, transfer or otherwise dispose of, directly and indirectly, all or substantially all of our assets to one or more third parties in any transaction or series of related transactions, including the sale of Yandex Russia, is also subject to the prior approval of the holder of the Priority Share. The Priority Share does not carry any rights to control the management or operations of the Company, and its economic rights are limited to its pro rata nominal entitlement to dividends and other distributions (a maximum distribution of one eurocent annually).

Yandex has also authorized, but has not issued, a class of preference shares. These shares are intended to serve as an anti-takeover measure, and could, for example, be issued to a protective foundation for the

purposes of making a hostile takeover of the Company impossible or undesirable. The Board believes that this additional protective measure will no longer be necessary in light of the proposed Restructuring, and the shareholders are now being asked to agree to amend the Articles of Association so as to no longer authorize this class of shares.

Risk Factors

The Board believes that the corporate governance changes it is proposing are targeted in nature and proportionate in addressing the concerns the Board has identified. However, these proposals will result in significant changes to our corporate governance, including through the powers granted to the Public Interest Foundation. See Section 5 of this Shareholder Circular for a description of some of the risks relating to the proposed Restructuring.

2. DETAILED DESCRIPTION OF THE PROPOSED RESTRUCTURING

This section contains a detailed summary of the main features of the proposed Restructuring.

Public Interest Foundation

A key element of the proposed structure is a new legal entity to be formed in Russia, the Public Interest Foundation. This entity will be formed in the Oktyabrskiy special administrative region in Kaliningrad. The applicable law governing the Public Interest Foundation has recently passed its third reading in the State Duma, which means it is now in final form, and is expected to be considered by the upper chamber of the parliament, the Federation Council, in the coming weeks and if approved, to be submitted to the President of the Russian Federation for signature by the end of 2019.

The Public Interest Foundation will hold the Priority Share (with its terms and rights amended as described above) in Yandex N.V., as well as the Special Voting Interest in Yandex Russia. Together, these will provide the Public Interest Foundation with certain important but targeted rights in relation to the ongoing corporate governance of the Yandex Group. The Priority Share may not be transferred without the prior approval of the Board, acting by a majority of eight directors (including one Designated Director). Transfer of the Special Voting Interest will be expressly restricted by Yandex Russia’s charter.

The Public Interest Foundation will have no shareholders, owners or beneficiaries, and will be governed by a board of directors operating under its charter. The Public Interest Foundation will not be permitted by its charter to engage in any commercial activities and its operating costs will be covered by the Company.

The effectiveness of the Restructuring is subject to, and conditional on, the final adoption of the Foundation Legislation.

Funding of the Public Interest Foundation

The Company will provide initial funding to cover ten years of expenses of the Public Interest Foundation and will extend a corporate guarantee to secure coverage of its normal operating costs. We do not expect such funding to exceed $200,000 annually.

Board of the Public Interest Foundation

The Public Interest Foundation will be governed by the Foundation Board. As set out in the Foundation Charter, the Foundation Board will be composed of 11 members, consisting of University Directors, Institutional Directors and Management Directors, as defined below.

The University Directors

Initially, five of the 11 directors will be nominated by Russian academic institutions (the “University Directors”). Each institution listed below will have the right to appoint one University Director to the Foundation Board. The academic institutions will be able to appoint and remove their directors at their discretion, provided their nominees meet the Eligibility Criteria (set out below).

· Moscow Institute of Physics and Technology (“MIPT”);

· Moscow State University (“MSU”);

· National Research University “Higher School of Economics” (“HSE”);

· Saint Petersburg University (“SPbU”); and

· University of Information Technologies, Mechanics and Optics (“ITMO”).

The Institutional Directors

Three of the 11 directors will be nominated by specified non-governmental institutions (the “Institutional Directors”). Each such institution will have the right to appoint one Institutional Director to the Foundation Board, subject to compliance with the Eligibility Criteria. Any replacement of an Institutional Director must be approved by at least two of the University Directors and at least two of the Management Directors. If one of the Institutional Directors ceases to hold office, the vacant position of the Institutional Director will be temporarily occupied by the head of the relevant institution until a new candidate is approved. The Management Directors and University Directors will use their best efforts to appoint a replacement Institutional Director within 30 days of the office becoming vacant. The named non-governmental institutions are:

· Moscow School of Management SKOLKOVO;

· Russian Union of Industrialists and Entrepreneurs; and

· Moscow School No. 57 Alumni Fund.

The Management Directors

Initially, three of the 11 directors will be members of Yandex Group management (the “Management Directors”), as follows:

· one of the three Management Directors will be Mr. Volozh, in his capacity as our CEO, and thereafter it will be our CEO from time to time or another executive director if there is no CEO then in office; and

· two senior managers of the Yandex Group, as selected by the director referred to above.

Future Composition of the Foundation Board

After Russian parties (including Russian citizens, Russian beneficially owned legal entities and the Volozh Family Trust) cease to hold cumulative voting power over at least 50% plus one vote in Yandex N.V., the number of Management Directors entitled to sit on the Foundation Board will be decreased from three to two. When this happens, the Management Directors will be the CEO or another executive director of the Company and a senior manager of the Yandex Group. In this case, the number of University Directors will increase from five to six as one additional director will be appointed by the Higher School of Economics. As a result, the University Directors’ votes will be sufficient to decide on the following matters without any additional votes by Management Directors or Institutional Directors:

· selection of candidates for binding nomination as Designated Director; and

· proposals of candidates for inclusion on the list of persons who may serve as Interim General Director from time to time.

Yandex’s Relationships with the Universities and Institutions

We believe that the representation of the named universities and non-governmental institutions on the Foundation Board will provide a valuable opportunity for us to gain insights into broader concerns about the public interest in our principal markets through their focused participation in certain aspects of our corporate structure. We have close and long-standing academic and business relationships with each of these entities, including those described below.

In 2007, Yandex founded the Data Analysis School, an educational institution with classes held directly at Yandex Campus and lectures given by both professors of various educational organizations and Yandex’s employees. As Mr. Volozh was the head of department of data analysis at MIPT at the time, MIPT naturally became the first university to start cooperation with the Data Analysis School, followed by HSE in 2008, and MSU and SPbU later on. Such cooperation is mutually important and sustainable, as the universities are able to increase their application rates by offering students unique opportunities to learn from Yandex’s leading industry expertise, while Yandex relies on the universities in its search for talent.

MIPT

· In 2007, Yandex founded a department of data analysis at MIPT that offers its students the opportunity to attend all core-specialty classes at the Data Analysis School. Mr. Volozh was the head of that department from 2007 until 2017; since 2019, it has been headed by Ms. Elena Bunnia (the General Director of Yandex Russia).

· The cooperation between Data Analysis School of Yandex with the School of Applied Mathematics and Computer Science of MIPT in 2011 developed further into offering students a dual-grade Master’s program in data search and machine learning.

· For over ten years, Yandex has been sponsoring the prestigious International Collegiate Programming Contest (“ICPC”) competitions held by MIPT and supported a number of MIPT’s team participating in the competitions.

HSE

· Yandex’s cooperation with HSE started in 2008, with a Master’s program in data analysis, where a large part of the curriculum was provided through Data Analysis School.

· In 2011, Yandex founded, under Yandex brand, a big data and information retrieval school at the Department of Applied Mathematics and Informatics at HSE.

· In 2014, Yandex and HSE co-founded the Faculty of Computer Since, which has set records for application rates since then.

· In 2015, Yandex founded a research laboratory dedicated to big data analysis in cooperation with the CERN, and is supporting multiple research projects by other laboratories.

· Mr. Volozh is a member of the Board of Trustees of the HSE and Chairman of that institution’s School of Computer Science, and Ms. Bunina was appointed to HSE’s supervisory board in 2019.

MSU

· MSU’s teaching staff represents a fair portion of teaching staff at the Yandex’s Data Analysis School. Since 2012, MSU and Data Analysis School offer dual-degree programs for the students of the MSU’s Faculty of Mathematics.

· Ms. Bunina has been a professor at Moscow State University since 2001. A substantial number of top managers of Yandex are graduates of MSU.

· Yandex is an active contributor to MSU’s MBA program run by the Graduate School of Management and Innovation.

SPbU

· In 2014, Yandex’s Data Analysis School and SPbU co-founded a Master’s program in data analysis.

· In 2019, Yandex co-founded a new Faculty of Mathematics and Computer Science. The faculty offers a brand new bachelor program developed by Yandex and the Data Analysis School.

· Yandex established a scholarship for outstanding students in the Mathematics, Algorithms and Data Analysis course.

ITMO

· Yandex has had an academic collaboration with ITMO’s renowned Computer Technology Department, which has evolved into a recognized Faculty of Information Technology and Programming.

· For over a decade, Yandex has been sponsoring the ITMO-organized ICPC World Programming Championship semi-finals. In addition, Yandex also supports quarter-finals in St. Petersburg and the National Programming Olympiad for Student Teams, also organized by ITMO.

Moscow School of Management SKOLKOVO

· The Moscow School of Management SKOLKOVO is a private business school founded in 2006 as a joint project of the national and international businesses.

· Our collaboration with SKOLOVO includes joint conferences and courses. Yandex is also supporting SKOLKOVO in development of online courses.

· Our Board member, Mr. Alexander Voloshin, is the Chair of the Board of Directors of Moscow School of Management SKOLKOVO.

Moscow School No. 57 Alumni Fund

· School No. 57 is one of the leading mathematical schools in Russia, one of Russia’s top ten schools by the number of national academic competition winners.

· Yandex has a long history of collaboration with School No. 57, which started in 2016 with the launch of Yandex.Lyceum as a testing ground for our educational projects.

· General Director of Yandex Russia, Ms. Elena Bunina, is a School No. 57 graduate. She has been teaching mathematics to senior year students at this school for 15 years.

Russian Union of Industrialists and Entrepreneurs (“RSPP”)

· Yandex is an active member of RSPP, an association for leading blue-chip Russian companies.

We believe that the broad and diverse membership of the Foundation Board, including members of management, will provide a balanced approach that will constructively consider the interests of our various stakeholders.

Appointment of Foundation Board Members

The Foundation Charter includes detailed provisions regarding the appointment, removal and replacement of the Foundation Board directors. Any amendment to the appointment mechanisms for the Foundation Board members requires the Company’s consent and approval of the Foundation Board, acting unanimously.

Priority Share

The Priority Share is currently held by Sberbank. As part of the proposed Restructuring, Yandex will repurchase the Priority Share from Sberbank for its €1.00 nominal value, and then transfer the Priority Share to the Public Interest Foundation, subject to shareholder approval of the Restructuring.

In addition, Sberbank will undertake to vote its Priority Share at the EGM in favor of the proposed Restructuring before it transfers the Priority Share.

Under the existing Priority Share, the holder has the right:

· to approve the accumulation by a party, group of related parties or parties acting in concert, of the legal or beneficial ownership of shares representing 25% or more, in number or by voting power, of the outstanding Class A and Class B Shares (taken together), if the Board has otherwise approved such accumulation of shares; and

· to approve a decision of the Board to sell, transfer or otherwise dispose of, directly and indirectly, all or substantially all of our assets to one or more third parties in any transaction or series of related transactions, including the sale of Yandex Russia.

It is proposed that the existing Priority Share will be transferred to the Public Interest Foundation and its terms will be amended to provide the new holder with the following rights (with the new provisions in bold italics):

· to approve the accumulation by a party, group of related parties or parties acting in concert, of the legal or beneficial ownership of shares representing 10% or more, in number or by voting power, of the outstanding Class A and Class B Shares (taken together), if the Board has otherwise approved such accumulation of shares. The accumulation threshold will be lowered from 25% (as it currently is) to 10%;

· to approve a decision of the Board to sell, transfer or otherwise dispose of, directly and indirectly, all or substantially all of our assets to one or more third parties in any transaction or series of related transactions, including the sale of Yandex Russia; and

· to make binding nominations of two Designated Directors, as described above.

Any amendment that affects the rights of the Priority Share will require the approval of the holder of the Priority Share.

Special Voting Interest in Yandex Russia

The Special Voting Interest in Yandex Russia represents an immaterial 0.001% interest in the charter capital of Yandex Russia and is designed solely for the purpose of ensuring an additional protection for the Public Interest Foundation functions. This participation interest entitles the Public Interest Foundation to remove the Yandex Russia General Director on a temporary basis in certain defined circumstances. This removal right may be triggered in only two types of situations: (1) a Special Corporate Situation; and (2) a Special Situation related to a matter of national security, which we describe in more detail below.

Eligibility Criteria

The University Directors and Institutional Directors must satisfy the following agreed requirements (the “Eligibility Criteria”):

· within the prior two years, they should not have been a political appointee or member of the governing body of a political party, a government official or a member or employee of any state apparatus, a member of parliament, or a political office-holder;

· they should have no criminal record, not be subject to professional disqualification under the Code of Administrative Offenses of the Russian Federation or administrative penalty for any offense listed in chapter 15 of the Code of Administrative Offenses of the Russian Federation;

· they should not be a person with whom Yandex or the Public Interest Foundation is restricted by law from conducting business;

· they should not currently be an employee of a state corporation or other company controlled by the state (or any state agency); and

· they and their family members and members of their household should not and have not had for the preceding two full calendar years any commercial conflict of interest.

With respect to the last item of the Eligibility Criteria, a director must disclose any conflict of interest, including if it arises after their election. In such case, the Company, as well as any Management Director or University Director, may initiate the process of removal of such director from the Foundation Board; removal in this manner will be deemed effective 20 days from the date of that notice. If there is a disagreement as to whether or not the Eligibility Criteria are satisfied, an independent expert from among the “Big Four” accounting firms can be asked to resolve the matter.

The satisfaction of the Eligibility Criteria by a candidate proposed by one of the non-governmental institutions will be mutually considered by the Management Directors and the University Directors before such candidate’s appointment. The Foundation Board will be able to waive one or more of the Eligibility Criteria in respect of a specific candidate by a resolution of at least two of the University Directors and at least two of the Management Directors.

The Yandex N.V. Board

Pursuant to the Articles of Association of the Company, the Board will consist of 12 members, of whom two will be Designated Directors nominated by way of binding nomination by the Public Interest Foundation as holder of the Priority Share. The same Eligibility Criteria will apply to the Designated Directors as to the members of the Foundation Board.

The remaining ten members of the Board will be nominated by the Nominating Committee, pursuant to the provisions described below.

The proposed amendment to the Articles of Association as part of the proposed Restructuring will increase the maximum terms of Yandex directors from three years to four. We believe that this change will provide greater stability for the oversight of our Company over the long term.

Initial Designated Directors

The Board is proposing for election at the EGM the following two persons to serve as the initial Designated Directors:

· Alexey Komissarov

· Alexei Yakovitsky

See section 3 of this Shareholder Circular for biographical information regarding these individuals.

Nominating Committee

The Nominating Committee will consist of five directors and will form two subcommittees.

Subcommittee I will consist of one Designated Director, one director with a Russian passport and residency, and one other Director. Subcommittee I will recommend to the Board for nomination four directors to the Board (the “Class I Directors”), which will then be subject to the approval of the Board as a whole. The Designated Director will have the right to veto any candidates for such slots, provided that the exercise of such veto has first been approved by the Foundation. The initial Class I Directors are Herman Gref, Mikhail Parakhin, Charles Ryan and Ilya Strebulaev.

Subcommittee II will consist of three directors who are not Class I Directors and will, by simple majority, recommend to the Board for nomination six directors (the “Class II Directors”); the Designated Directors will have no right of veto over candidates for these seats. The Board must adopt the recommendations of

candidates recommended by Subcommittee II, unless the Board votes by a supermajority of ten Directors (subject to adjustment for Board vacancies) to reject such recommendation.

Public Interest Committee

Certain targeted and defined actions in respect of material intellectual property or personal data will require the prior approval of the Public Interest Committee (see below). The Public Interest Committee will consist of three members: the Yandex CEO and both of the Designated Directors, and its decisions must be unanimous. The Public Interest Committee is not empowered to review ordinary business or commercial matters.

If the Public Interest Committee does not approve the matter referred to it, the Board will follow the decision of the Public Interest Committee not to authorize such matter, unless the Board rejects such decision by either (i) a supermajority of eight votes (subject to adjustment for Board vacancies), which shall include the affirmative votes of the two Designated Directors; or (ii) a supermajority of eight votes (subject to adjustment for Board vacancies) (not including the affirmative votes of the two Designated Directors) provided that the Foundation Board has given its approval. The Public Interest Committee will act only as a check on the Board’s actions; it cannot proactively make any decisions on behalf of the Board or require the Board to take any action.

Competence of the Public Interest Committee

The following are the matters that will require the approval of the Public Interest Committee:

· transactions or other transfers resulting in the granting of direct access to Russian users’ personal data owned by us and non-depersonalized big data owned by us to non-Russian persons;

· the adoption, modification, amendment, and cancellation of the Yandex internal policies on protection of personal data and non-depersonalized big data of Russian users (including storage procedures, and sale/provision of such information to foreign persons);

· entry by the Company into any agreement which concerns Russia with a non-Russian state or a international intergovernmental organization (or its bodies and agencies); and

· direct or indirect transfers or encumbrances of material intellectual property rights, including licensing such rights, if as a result of such license the Company would lose the ability to use such rights in Russia.

Special Voting Interest in Yandex Russia

As an additional protection for the overall structure, the Public Interest Foundation will hold a Special Voting Interest in Yandex Russia, which will provide limited and defined powers that will be exercisable only in the case of what we describe as a Special Corporate Situation or a Special Situation related to a matter of national security (each, the “Relevant Situation”). We believe that the issuance of the Special Voting Interest in Yandex Russia to the Public Interest Foundation, giving the Public Interest Foundation the right in certain defined and targeted circumstances to replace, on a temporary basis, the General Director of our principal Russian operating subsidiary, should effectively provide comfort to the public authorities that this protective structure is not entirely reliant on resolution outside of Russia.

The Relevant Situations will provide a special ground for the termination of the employment of the General Director. The defined circumstances in which this power will arise is set out in the charter of Yandex Russia, which is a public document, and are described below.

Special Corporate Situations

A Special Corporate Situation is deemed to arise only in the following specific circumstances:

· the Public Interest Committee is not formed;

· the Public Interest Committee is dismissed by the Board;

· a Designated Director is not included in the Nominating Committee;

· a binding nomination for a Designated Director is rejected by the Company’s General Meeting;

· a Designated Director is removed by the Company’s General Meeting without approval of the holder of the Priority Share;

· the General Meeting of Yandex appoints a candidate as a Class I Director that has not been recommended by the Nominating Committee through Subcommittee I; or

· a decision of the Public Interest Committee is breached by Yandex Russia.

If the Foundation Board decides that any of the above triggers for a Special Corporate Situation has occurred, it must send a notice to the Company. This will require the approval of five University Directors and one additional vote of an Institutional Director or a Management Director. That notice must clearly indicate the trigger for a Special Corporate Situation. Following receipt of such notice, the matter may be cured by the Company, and Yandex Russia if applicable, by taking appropriate corporate actions that are within the powers of the Company and Yandex Russia as clearly defined in the charter of Yandex Russia. The cure period is dependent on the particular trigger for the Special Corporate Situation and provides the Company, and Yandex Russia if applicable, an opportunity to eliminate the trigger before the next regular Board meeting, the next regular shareholders meeting, or until the expiry of a period of 60 days from the date of the relevant notice from the Public Interest Foundation (as specified for each trigger of the relevant Special Corporate Situation in the charter of Yandex Russia).

If the Company and Yandex Russia do not eliminate the trigger for the Special Corporate Situation after the relevant cure period has expired, the Public Interest Foundation may by the votes of five University Directors and one additional vote of an Institutional Director or a Management Director resolve that the Special Corporate Situation is pending and call a general meeting of Yandex Russia’s participants to dismiss the then-acting General Director and appoint an Interim General Director.

The Foundation’s Special Voting Interest in Yandex Russia becomes “super-voting” on this matter. This means that the Public Interest Foundation will have the ability to replace the General Director of Yandex Russia without the vote of Yandex N.V. The Public Interest Foundation will appoint an Interim General Director from the pre-approved list, in accordance with the charter of Yandex Russia.

As soon as the situation is resolved in accordance with the procedure set out in the charter of Yandex Russia, the Company as the holder of the majority interest in Yandex Russia will remove the Interim General Director and appoint a permanent General Director. The permanent General Director may be the former General Director, in which case no additional Board approval of the candidacy of such General Director will be required, or a new permanent General Director, if the Board resolves not to reinstate the former General Director by the vote of a supermajority of eight (as may be adjusted for any Board vacancies) increased with one affirmative vote.

Special Situations related to a matter of national security

A Special Situation is a matter constituting an extraordinary one-off event related to matters of the national security of the Russian Federation requiring quick remedy.

If the Foundation Board decides that a Special Situation has occurred it must send a notice to management of the Company and Yandex Russia specifying the particular violation that the Foundation Board considers to constitute a Special Situation relevant to national security. This will require the approval of five University Directors and two additional votes from either Institutional Directors or Management Directors. That notice must provide for a period of at least seven days for such potential Special Situation to be cured or averted.

The Public Interest Foundation may, at its discretion, by the vote of five University Directors and two additional votes from either Institutional Directors or Management Directors, resolve upon the expiry of the cure period that the Special Situation is pending and call a general meeting of Yandex Russia participants to dismiss the acting General Director and appoint an Interim General Director.

The Public Interest Foundation’s Special Voting Interest in Yandex Russia becomes “super-voting” in this event. This means that the Public Interest Foundation will have the ability to replace the General Director of Yandex Russia. The Public Interest Foundation will appoint an Interim General Director, in accordance with the charter of Yandex Russia.

The Interim General Director so appointed due to a Special Situation will hold office for 15 days. Upon the expiration of such 15-day period (or earlier, if the Board and the Public Interest Foundation mutually agree that the relevant Special Situation has been resolved) the Company as the holder of the majority of votes in Yandex Russia will appoint a permanent General Director of Yandex Russia. If the person nominated to be permanent General Director is the former General Director then no additional Board approval of the candidacy of such General Director will be required. If the Board resolves not to reinstate the former General Director by a special majority of nine (as may be adjusted for any Board vacancies) a new General Director may be appointed.

The Foundation Board is not entitled to adopt repeated decisions on the occurrence of a Special Situation in connection with the same violation related to a matter of national security.

General Director of Yandex Russia

The General Director of Yandex Russia will be appointed in the normal course of business by Yandex, as the majority participant in Yandex Russia, subject to a resolution by the Board made by a special majority of eight (as may be adjusted for any Board vacancies), including at least one Designated Director. If a Designated Director vetoes five proposed candidates, then the next proposed candidate may be selected by the Board upon the approval of the special majority of nine (as may be adjusted for any Board vacancies) and the vote of a Designated Director will not be required.

In connection with the Restructuring, the charter of Yandex Russia will be amended to limit the powers of the General Director in the ordinary course. Accordingly, certain actions on behalf of Yandex Russia will be subject to the approval of the general meeting of participants, including the following:

· entering into transactions with any governmental authorities or with any entity owned or controlled by the state;

· transactions exceeding RUB 3,000,000 (approximately $47,000 as of the date hereof) individually, or RUB 30,000,000 (approximately $470,000) in aggregate during one month;

· entering into transactions related to any borrowings, provision of any guarantees or indemnities; and

· amending the staffing schedule.

Previously, no requirement to obtain consent of the Company for those actions was envisaged for the General Director by the charter of Yandex Russia.

Powers of Interim General Director

The charter of Yandex Russia includes a specific and exclusive list of powers that may be exercised by an Interim General Director appointed as a result of a Special Corporate Situation or a Special Situation. This list of powers is significantly more limited than the powers ordinarily afforded to the General Director, reflecting the interim nature of the appointment and that the appointment is for a specific purpose (being to manage the exceptional circumstances that have led to his appointment). In particular, the Interim General Director is not authorized to terminate employees, manage the bank accounts of Yandex Russia or enter into significant transactions.

The Interim General Director will report to the general meeting of participants in Yandex Russia (i.e., the Company and the Foundation) and may not take actions on any matters reserved for the general meeting, which is controlled by Yandex N.V. Accordingly, all material matters will require the approval of Yandex N.V. However, the Interim General Director will have the power, without a prior approval from the Company, to:

· enter into a single transaction not exceeding RUB 3 million (approximately $47,000) or a series of related transactions not exceeding RUB 30 million (approximately $470,000) in aggregate on a monthly basis;

· challenge transactions and hire outside counsel for litigation within a limit of RUB 10 million (approximately $157,000);

· enter into legal services agreements with high-ranking legal counsel for an amount not exceeding RUB 10 million (approximately $157,000) and issue and revoke powers of attorney for court representation to such legal counsel, and

· impose disciplinary penalties on Yandex Russia employees.

The financial authority of the Interim General Director is limited and requires that any expenditure of Yandex Russia’s funds, borrowings or extension of loans be co-signed by the financial director of Yandex Russia.

List of Candidates for Interim General Director

In the course of proposed Restructuring, at least three alternative/successor candidates will be agreed upon to serve as Interim General Director of Yandex Russia, each of whom will meet the Eligibility Criteria and will be available to become an Interim General Director from time to time.

Going forward, a list of candidates to serve as Interim General Director will be supplemented by the Company as the holder of the majority votes in Yandex Russia, subject to a supermajority vote (eight out of 12 Directors, subject to adjustment in the case of Board vacancies), provided however that both Designated Directors vote in favor. If both Designated Directors are unavailable, the Board may make a decision with the consent of the Public Interest Foundation.

To ensure that there is always a candidate for Interim General Director, if at any time:

· only two candidates remain on the list and the Company cannot appoint a new candidate within 120 days, such candidate will be appointed by a majority vote of the Foundation Board, subject to the Eligibility Criteria;

· only one candidate remains on the list and the Company cannot appoint new candidates within 60 days, up to two candidates will be appointed by a majority vote of the Foundation Board, subject to the Eligibility Criteria; and

· no candidates remain on the list and the Company cannot appoint at least one candidate within 15 days, such candidate will be appointed by a majority vote of the Foundation Board, subject to the Eligibility Criteria.

Once at least one candidate is added to the list, the Company will again have the power to appoint further candidates by its majority vote subject to the above terms.

Volozh Family Trust; Lock-up Agreement

As part of the proposed Restructuring, we are proposing an amendment to the automatic conversion feature of the Class B Shares.

Under the current articles, our Class B Shares would automatically convert into Class A Shares immediately upon the death of the holder, including Mr. Volozh. To avoid this “cliff edge” scenario, in which the voting control of the Company could suddenly shift, the proposed amendment to the Class B Shares would provide that any Class B Shares held by a family trust would not automatically convert for a period of two years following the holder’s death. The proposed amendments are intended to ensure an orderly transition period, and is similar to the structures that have been adopted by other public technology companies, such as Crowdstrike, Dropbox, Lyft, Pinterest and Snap.

Mr. Volozh anticipates establishing a family trust prior to the implementation of the proposed Restructuring. During the two-year transition period following the death of Mr. Volozh, the trustee of the Volozh Family Trust will be bound to vote in favor of any proposal of the Board, and in accordance with the Board’s recommendation on any other matter. These restrictions will fall away, and the Class B Shares will automatically convert into Class A Shares, after the end of that two-year period pursuant to the Articles of Association.

Lock-Up Agreement

Mr. Volozh and the Volozh Family Trust intend to enter into a lock-up agreement in favor of the Company with respect to 95% of the Class B Shares currently held by Mr. Volozh, pursuant to which they will undertake not to dispose of such shares prior to January 1, 2022. Even if the other holders of Class B Shares were to sell their shares and Mr. Volozh sold the permitted 5% of his Class B Shares, he would still hold over 51% of votes in the Company and, as such, control would remain in Russian hands during this period.

Mr. Volozh is not currently subject to any lock-up restriction in respect of his Class B Shares. He has agreed that he, and his family trust, will enter into such restriction to demonstrate his commitment to the Company and provide an additional layer of assurance that there will be no abrupt change in the voting structure of our Company.

The lock-up agreement will provide that such restrictions may be waived or released by our Board, acting by a supermajority of eight (8) Directors, subject to adjustment in the case of Board vacancies.

Amendments to the Articles of Association of Yandex

In accordance with the proposed Restructuring, the Board is proposing that the Yandex shareholders approve amendments to the Articles of Association of Yandex. A separate vote of the Class A Shareholders will take place prior to the EGM. Our shareholders are advised to consider the amendments contained in the draft Deed of Amendment of the Articles of Association. For convenience, certain key amendments are summarized below:

· The rights attaching to the Priority Share are being amended. The holder of the Priority Share will have the right to make a binding nomination for the appointment by the General Meeting of two Non-Executive Designated Directors (see below), in addition to rights in respect of the accumulation of large stakes (with the threshold being reduced from 25% to 10% of the voting rights or number of Class A Shares and Class B Shares) in the Company, and the approval of the sale of substantially all of the Company’s assets. The Priority Share may only be held by the Public Interest Foundation or another party specifically nominated by the Board for this purpose.

· The two Non-Executive Directors who will be appointed on the basis of a binding nomination by the holder of the Priority Share will form a separate class of Designated Directors. One Designated Director will be a member of the Nominating Committee and both Designated Directors will be members of the Public Interest Committee.

· The holder of the Priority Share will be entitled (1) to request the Board to call a General Meeting to fill a vacancy in respect of one or both Designated Directors, (2) to propose specific items for the agenda of the Annual General Meeting (such as a proposal to remove a Designated Director from office and, subject to and conditional upon the approval by a General Meeting of such removal, a binding nomination of a replacement Designated Director) and (3) once every calendar year to call a General Meeting solely for purposes of proposing the removal of a Designated Director and the election of a replacement Designated Director.

· Any amendments to the Articles of Association which affect the rights of the Priority Share, including, but not limited to: (i) the size of the Board, (ii) the Eligibility Criteria, (iii) the Nominating Committee; or (iv) the Public Interest Committee, will require the prior approval of the holder of the Priority Share.

· Each Director will have to meet Eligibility Criteria and certain Directors will have to meet Independence Criteria (as defined in the Articles of Association).

· The General Meeting may appoint substitute Directors in the event one or more Directors ceases to hold office or is unable to execute his/her duties and responsibilities during such period of absence until a new Director has been appointed. The appointment of substitute Directors may be made at any time including at the time of the appointment of the original Director. A substitute Designated Director shall be appointed on the basis of a binding nomination by the holder of the Priority Share.

· Any resolution by the Board taken at a meeting shall require the affirmative votes of at least seven (7) Directors (if the Board of Directors consists of eleven (11) Directors or more) or six (6) Directors in case the Board of Directors consists of seven (7), eight (8) or nine (9) Directors (or if the Board of Directors consists of less Directors, such lesser number as are then in office) present or represented at such meeting, unless the Articles of Association provide otherwise; and certain resolutions by the Board can only be taken with certain majorities which in certain circumstances has to include the affirmative votes of one or more Designated Directors.

· The appointment by the Board of a Chief Executive Officer requires the affirmative vote of at least eight (8) Directors (excluding the vote of the Director who is being considered for the position).

· The following new committees of the Board will be established and existing committees of the Board will be formally established in the Articles of Association:

· Public Interest Committee (new);

· Nominating Committee (new); formerly constituted as part of the Nominating and Corporate Governance Committee;

· Corporate Governance Committee (new); formerly constituted as part of the Nominating and Corporate Governance Committee

· Audit Committee (existing); and

· Compensation Committee (existing).

· The provision in the Articles of Association that provides that qualified shareholding restrictions for holders of ordinary shares will terminate if any law or regulation of the Russian Federation is adopted which imposes a limitation or restriction on the ownership of internet business in Russia by non-Russian parties, will be deleted. This means that if foreign ownership laws are adopted in Russia that are applicable to our Company, the veto right of the Priority Share over the accumulation of a stake of more than 10% in our Company will continue in force, rather than terminate.

· Any resolution of the General Meeting to issue Class A Shares or Class B Shares or to delegate the authority to issue Class A Shares or Class B Shares to another corporate body, will require the prior approval of the Meeting of holders of Class A Shares if the issue of Class A Shares or Class B Shares exceeds 20% of the issued share capital of the Company.

· Any resolution by the Board (1) to transfer the enterprise or substantially all of the enterprise of the Company to a third party, (2) to conclude or cancel a long-lasting cooperation that is of essential importance to the Company, (3) to acquire or dispose of an interest in the capital of a company with a value in excess of one-third (1/3) of the total consolidated assets of the Company or (4) to enter into a transaction or series of related transactions by the Company or a subsidiary involving the payment of an amount in excess of one-third (1/3) of the total consolidated assets of the Company or the sale of assets in excess of that amount, will require the prior approval of the Class A Meeting.

· Any resolution of the General Meeting to amend the Articles of Association, to conclude a legal merger or demerger or to dissolve the Company will require the prior approval of the Meeting of holders of Class A Shares.

· The automatic conversion mechanism for Class B Shares is being amended in that Class B Shares held by a family trust will not automatically convert into Class A Shares until the end of a period of two (2) years following the holder’s death.

· The automatic conversion mechanism for Class B Shares if and when 95% or more of all issued and outstanding Class A Shares and Class B Shares (by number, taken together) are Class A Shares, will be deleted.

· A technical amendment to eliminate the preference shares from the authorised share capital of the Company.

· The authorised share capital of the Company is being amended as set out in the draft Deed of Amendment of the Articles of Association.

· The threshold for shareholders to propose agenda items for a General Meeting will be increased to at least 3% (from at least 1%) of the issued share capital of the Company and the alternative market value threshold of EUR 50 million will be deleted.

· The right of shareholders together holding at least 10% of the issued share capital of the Company to request the Board to call a General Meeting, will be made subject to court approval.

3. INITIAL DESIGNATED DIRECTORS

Assuming the proposed Restructuring is approved, we expect that the appointing parties specified above will select their initial representatives to sit on the Foundation Board. Going forward, the Foundation Board will select candidates to be proposed from time to time by way of binding nomination for election as Designated Directors on the Board of Yandex.

Although the Foundation Board has not yet been formed, we understand from the relevant universities and non-governmental institutions that the preferred initial candidates for nomination as Designated Directors have been identified. Accordingly, the Board is proposing for election at the EGM the following two persons to serve as the initial Designated Directors, each for an initial term ending at the Annual General Meeting of shareholders ending in 2023:

· Alexey Komissarov (age 50) is vice-rector of the Russian Presidential Academy of National Economy and Public Administration. He is also a member of PJSC SIBUR Holding’s board of directors. From 2015 to 2017, he was director of the Industry Development Fund and served as independent director, member of the Strategy and Investment Committee and chairman of the Budget and Reporting Committee to GLONASS. From 2011 to 2015, he worked in the Moscow government as a minister and head of the Department of Science, Industrial Policy and Entrepreneurship, and also served as advisor to the Mayor. Mr. Komissarov has a degree from the Moscow Automobile and Road Construction State Technical University in Automotive Engineering and Maintenance, and an MBA from Kingston University in the UK.

· Alexei Yakovitsky (age 44) is the CEO of VTB Capital, VTB Group’s investment banking business. He is also a member of VTB Capital’s board of directors. In addition, he is the chairman of the Supervisory Board of VTB Bank (Europe) SE, headquartered in Frankfurt, Germany. Mr Yakovitsky is also a member of the board of directors of VTB Capital Plc, VTB Capital’s London subsidiary and a member of the board of directors of Rostelecom. Mr. Yakovitsky started his career in equity research at United Financial Group (“UFG”). He was ranked the #1 telecom analyst for Russia by Institutional Investor in 2004 and was co-head of Russian equity research at UFG and Deutsche Bank (which acquired UFG) in 2005-2008. He then joined VTB Capital in 2008 as co-head of equities and head of research, and became its Moscow CEO in 2009. Mr Yakovitsky has degrees from Moscow Lomonosov State University, Department of History, as well as from the Nelson A. Rockefeller College of Public Affairs and Policy (Albany, US).

Although neither Mr. Yakovitsky nor Mr. Komissarov has a commercial conflict of interest with our Company, neither satisfied all of the Eligibility Criteria applicable to Designated Directors. Consistent with the provisions of our Articles of Association that will be effective following the implementation of the Restructuring, our Board considered the qualifications and experience of such individuals and determined to waive the applicable criteria in respect of these candidates.

4. GENERAL BACKGROUND TO THE PROPOSED RESTRUCTURING

The Yandex Group operates in a rapidly evolving environment of increasing regulatory complexity, reflecting a trend towards increasing scrutiny of large technology companies by policymakers, regulators and the general public in jurisdictions across the globe, including in Russia.

Scrutiny of technology companies by U.S. regulators

The United States government has been taking steps to regulate its technology market in recent years, including, for example, the following:

· In September 2019, the U.S. Treasury issued draft regulations to implement changes required under the Foreign Investment Risk Review Modernization Act 2018 (known as “FIRRMA”). The effect of the proposed changes would be to expand the number and type of investments and activities that will fall within the jurisdiction and scrutiny of the Committee on Foreign Investment in the United States (known as “CFIUS”) (being a committee chaired by the Secretary of the Treasury authorized to review certain transactions involving foreign investment in the United States). The U.S. government has taken steps to exclude Huawei from developing 5G networks in the United States based on perceptions of the Chinese government’s influence over Huawei. Limits have also been placed on U.S. companies working with Huawei. These developments come amidst reports that the Trump Administration is weighing the delisting of Chinese stocks as part of a broader protectionist agenda from the government.

· Similarly, CFIUS recently ordered the divesture of Beijing Kunlun’s ownership of the online dating site Grindr, opposing its plans for an initial public offering.

· In late November 2019, the U.S. Federal Communications Commission is expected to vote on the U.S. Attorney General’s proposal barring U.S. rural wireless carriers from purchasing, as well as requiring them to replace any telecommunications equipment produced by, Huawei and ZTE.

· CFIUS also blocked the proposed takeover by Broadcom Limited (a Singapore-incorporated company) of Qualcomm Incorporated (a US-incorporated company).